For many regional banks and credit unions, 2025 will feel like a line in the sand. The promise of GenAI and intelligent automation is no longer hypothetical; customers and new competitors expect faster, clearer experiences and back offices that cost less to run. At the same time, regulators want transparency. For a mid-market bank CIO or head of technology starting from limited AI maturity, the challenge is practical: how to move from experiments to operational value without tripping over governance, privacy, or reputational risk.

Executive brief: Why 2025 is the year to operationalize AI—carefully

Neobanks and big-tech experiences are resetting customer expectations. Meanwhile margin pressure from low rates and higher compliance costs means efficiency is now a strategic priority. This combination makes an AI strategy for banks urgent—but it must be built on explainability, auditability, and clear governance. Regulators will ask for decision logs, model documentation, and evidence that human oversight exists. Starting small and structured in 2025 lets mid-market institutions capture productivity gains while meeting those demands.

The 5 trends that matter most for banking leaders

Not every AI headline is relevant. The shifts that will shape practical deployments this year are focused and familiar: first, GenAI copilots that help employees draft credit memos, summarize KYC files, and answer policy questions; second, risk-aware intelligent automation that reduces friction across payments exceptions and reconciliations; third, AI-enhanced fraud and AML triage that prioritizes alerts while keeping analysts as decision-makers; fourth, the rise of data products and feature stores to make models reusable; and fifth, a move from ad-hoc model governance to policy-driven frameworks. Each trend supports faster outcomes, but all require controls.

Identify first-wave use cases with fast ROI and low regulatory risk

A pragmatic mid-market bank CIO roadmap begins with a tight portfolio of two to three use cases that demonstrate value quickly. Good candidates are high-friction, high-volume tasks where an assistant can reduce manual work without assuming full decision authority. Examples include onboarding and KYC document extraction (OCR plus structured outputs), lending operations summaries that prepare draft credit memos for underwriter review, and internal productivity tools like a policy Q&A copilot or automated call-note summarization. For fraud operations, focus on AML AI triage that ranks alerts so analysts can concentrate on true positives rather than replacing human judgment entirely.

Data readiness and guardrails: What’s enough to start

Data readiness is often the gating factor. You do not need a perfect data lake to begin; you need a secure, verifiable baseline. Centralize critical documents and transaction histories in locked repositories, apply masking where possible, and define retention policies up front. For GenAI use cases, adopt retrieval-augmented generation (RAG) so model outputs are grounded in your bank content rather than hallucinations. Log prompts, responses, and retrieval traces. Implement role-based access controls and maintain separate environments—sandbox, UAT, and production—to keep testing artifacts isolated from live systems.

Governance-by-design for regulated AI

Embedding governance from day one reduces rework. Start with a tiered model risk approach: classify models and copilots by impact, require approval checkpoints for medium- and high-risk systems, and use standard documentation templates and model cards for every deployment. Human oversight must be explicit: define who reviews flagged decisions, how escalations work, and what the fallback path is when the AI is uncertain. Align bias and performance testing to relevant guidance (FFIEC in the U.S., MAS or local regulators as appropriate) and keep audit trails that show inputs, outputs, and decision rationale.

People and process: Standing up a cross-functional AI squad

Small teams move faster than committees. Assemble a standing squad that includes a product owner from operations, a technical lead, a data scientist/engineer, and a risk or compliance representative. Run two-week sprints with a demo to stakeholders and tight feedback loops. The squad should measure outcomes—not lines of code—using KPIs like cycle time reduction, error-rate decline, and hours saved. Training and change management for analysts are as important as the models themselves; invest in role-based training and clear playbooks for how to use the new tools safely.

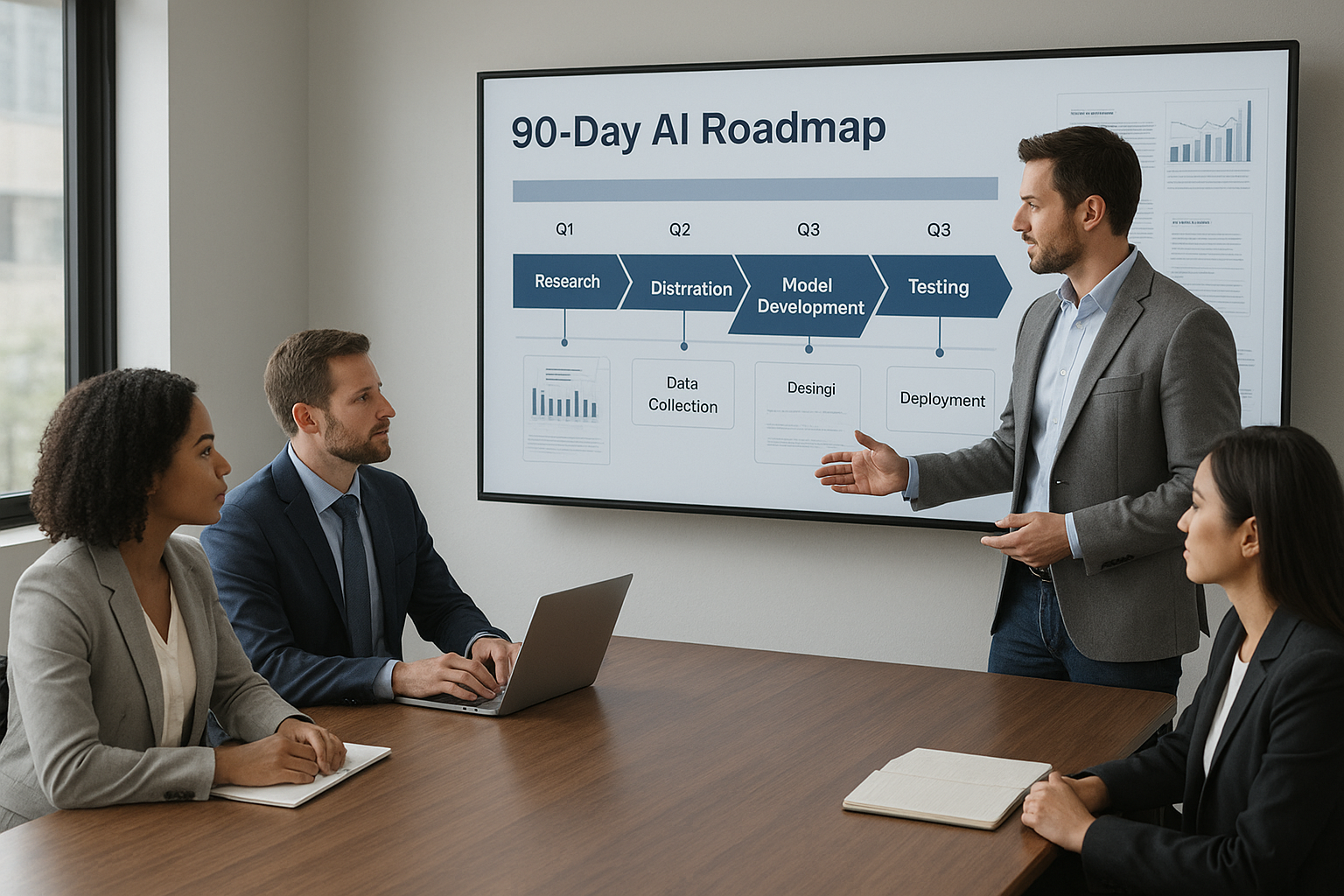

The 90‑day plan

Turn strategy into a week-by-week roadmap. Weeks 1–2 focus on use-case selection, risk categorization, and securing data access approvals. Bring legal and compliance into the room to avoid surprises. Weeks 3–6 are for prototyping: build narrow prototypes using synthetic or masked data, create RAG retrieval chains against known-document sets, and run initial governance checkpoints. Weeks 7–10 move into analyst UAT: have frontline staff use the tool in parallel with their normal workflow, collect feedback, and instrument monitoring for quality and safety. Weeks 11–13 are for limited production rollout to a subset of users, establishing monitoring, fallback procedures, and capturing ROI metrics for executive reporting.

Measuring ROI executives trust

Finance leaders want clear, auditable outcomes. Translate AI gains into CFO-friendly metrics: hours reallocated, reduction in case cycle time, fewer exceptions, and decreased false positives in fraud or AML AI triage. Complement efficiency metrics with quality metrics such as reduction in rework and improved decision accuracy. For compliance, present evidence bundles: decision logs, prompt and retrieval traces from RAG banking use cases, model cards, and test results that demonstrate consistent performance over time.

Build vs. buy: Choosing the right path for the first wave

Speed matters, but so does control. For a first wave, prefer a hybrid approach: assemble proven off-the-shelf components such as OCR and redaction tools and layer them with custom orchestration and business logic. Keep architecture modular so you can swap models or vendors as policies and technology evolve. Pilot in vendor sandboxes where possible, and negotiate clear data rights and exit clauses to preserve optionality. This balance helps a mid-market bank CIO move quickly without sacrificing governance.

How our team accelerates your start

For banks starting their AI journey, an external partner can help reduce discovery time and operational risk. Effective engagement focuses on rapid discovery to select compliant, high-ROI use cases; RAG-based GenAI blueprints and secure workflow automation for banking process automation; and a risk-aware MLOps setup that includes logging, monitoring, and analyst enablement. The objective in 90 days is not perfection but production-grade pilots that demonstrate measurable value and build the foundations of an AI strategy for banks that is both pragmatic and defensible.

Starting smart in 2025 means choosing a narrow set of outcomes, instrumenting governance from day one, and measuring what executives care about. For mid-market banks, that approach turns GenAI in financial services 2025 buzz into repeatable productivity and safer, faster operations.

Sign Up For Updates.